News

Jumia Technologies: Strong Performance Despite Global Economic Disruptions (Seeking Alpha)

May 14, 2026Company News

Last week’s earnings report for Jumia Technologies AG (JMIA) came at a time when the stock was struggling to recover from a poor reaction to Q4 earnings. The stock is down 38% year-to-date while the U.S. stock indices race from one all-time high to another. Yet Jumia’s execution has at least as much momentum as it did when the stock was challenging its 2024 high. CEO Francis Dufay declared in the company’s Q1 earnings conference call that “our momentum towards profitability is continuing and, in several important ways, accelerating.” Thus, hours after the company reported results on May 7, 2026, I went into my quarterly post-earnings interview with Dufay mainly focused on clarifying the finer points of the earnings report and presentation. I also wanted to understand how the company was able to deliver such a strong Q1 performance despite the disruptions in the global economy from the war against Iran. These dislocations represent a new risk landscape for the company and for investors.

Performance And Guidance Amid Uncertainty

Jumia hit the top end of its guidance for Q1 GMV growth of 27% to 32%, an impressive achievement since the quarter’s results included the month of March, when the war against Iran first disrupted the global economy. This growth was driven by strong performance across the business, including the following achievements listed in the Q4 earnings presentation (adjusted as needed for perimeter effects):

- Gross profit margin expanded by 160 basis points to 13.9% of GMV (driven by improved marketplace monetization).

- Quarterly cash burn decreased to $15.3M versus $23.2M in Q1 2025 (the liquidity position is now $62.6M).

- Adjusted EBITDA loss declined to $10.7M versus $15.7M in Q1 2025.

- Physical goods orders grew 31% year-over-year, and quarterly active customers grew 25% year-over-year.

- Repeat behavior improved from 45% of new customers in Q4 2024 making a repeat purchase within 90 days to 47% in Q4 2025 (there is a one-quarter lag in making these measurements).

Jumia also maintained guidance for the year. The company remains on track to achieve breakeven in Q4 and profitability for the full-year 2027. Thus, I wondered whether Q1’s surprising strength could translate into the potential for an upside surprise in future quarters. Dufay contextualized the forward guidance with a reminder that he cannot know what is going to happen in the global economy: “The guidance is based on what is currently known.” However, he added that “the assumption is that everything we’re seeing is temporary.” This conclusion is key to the short-term thesis for JMIA. The longer the war drags on, the larger the risk profile becomes.

While Jumia was able to hit guidance, the current economic uncertainty and volatility are pressuring prices for smartphones and fuel. The increase in the cost of memory has driven the price of cell phones up by 20%. However, Dufay noted that most people “need a (phone) period… People will just buy lower specs… Some people won’t be able to afford a smartphone anymore, so they buy a feature phone.” While he could not make a hard estimate of the demand shifts, he explained that margins are “pretty much the same” between smartphones and feature phones given the competitive market. The willingness of consumers to trade down their phones means Jumia can maintain volumes without a hit to the bottom line. However, in the next quarter’s earnings, I want to get detail on the share of consumers who get forced completely out of the market for phones. This number could be an early indicator of the health of consumer spending. Similarly, I will hone in on the retention data for Q1.

Fuel prices have increased significantly across the globe; Jumia’s African markets are no different. Dufay explained in the conference call that the company is absorbing the higher fuel costs through a surcharge in some countries. During our discussion, Dufay further explained that “at the end of the day, the willingness to pay is limited.” That is, there is little opportunity or capacity for consumers to absorb these higher prices to transport their purchases. However, Dufay insisted that the “fuel price is a headwind, but it doesn’t fundamentally change the medium-term picture.” I interpret the strong results in Q1 as initial validation of this outlook.

Either way, I am bracing for increasingly wary investors to demonstrate heightened sensitivity to Q2 results if they are impacted by deteriorating conditions in the global economy from the war against Iran. While Jumia’s business has been resilient in the past 3 years, the stock remains vulnerable to bouts of weakness driven by fears over short-term challenges.

Upcountry And Starlink

Jumia continues to expand outside of the major cities and into the “upcountry.” Orders from upcountry regions delivered 62% of total volume, up from 58% in Q1 2024 (both adjusted for perimeter effects). This growth in share is part of Jumia’s strong fundamentals. Upcountry expansion drove Jumia’s success in Ivory Coast and is a core story in Nigeria. An upcountry push is now driving growth in Kenya.

The upcountry growth is also expanding opportunity for Jumia’s partnership with Starlink. Strong Starlink sales in Nigeria and Kenya support first-party sales, which are now 46% of total revenue. Dufay indicated that Jumia is looking for opportunities to open more countries, given “it’s a very strong product to sell.” For example, the company is making progress on regulatory clearances in the Ivory Coast.

Starlink also brings a positive flywheel for the upcountry expansion. More accessible and reliable internet service is a cornerstone for e-commerce adoption. I hope that regulatory clearance in Ivory Coast will open up faster uptake in other countries as the economic benefits of connectivity motivate policy makers.

Ivory Coast Vs. Ghana

While Jumia makes progress on getting Starlink into the Ivory Coast, the recent collapse in the price of cocoa has impacted the economy there, and a supply disruption in appliances impacted growth in the quarter. These impacts are additive to the headwind of higher prices for smartphones. Despite these headwinds, Dufay issued a reassurance in the earnings conference call: “…we remain confident in the fundamentals of our business in Ivory Coast, where we hold a very strong position with a trusted brand and healthy monetization.” Still, the plunge in cocoa prices is a major economic hardship for cocoa farmers, so I will continue to follow this story as a macroeconomic force that could cause incremental downside risk to Jumia’s stock in Q2.

Ghana is also a major importer of cocoa, but its economy is more diversified than the Ivory Coast’s. Despite a 40% jump in fuel prices, business remained robust in Ghana, where physical goods GMV grew 142% year-over-year versus 65% a year ago. Still, Ghana is just 12% of Jumia’s physical goods GMV. Dufay describes the Ghanaian market as “under-penetrated.” This theme is familiar from previous earnings reports, and it makes sense. I have visited Ghana twice in recent years and have seen and experienced for myself the vibrancy of its economy. (As a side note, I used Jumia for food delivery on a trip to Accra, Ghana, in 2018, and afterwards put the company on my investing radar).

Electrifying Ugandan Distribution

Last September, Jumia partnered with Spiro to introduce delivery by e-bike in Uganda. This pilot program is gaining traction and producing results. Accordingly, Jumia wants to expand this program into other countries as part of an initiative to reduce the reliance on gasoline/diesel in logistics. Dufay explained that “across Africa, EVs make sense when you have high utilization…for deliveries like ours, it does make sense.” Electrifying the last mile delivery reduces unit costs because “electricity is cheaper than fuel, especially now, but even two months before.” The trade-off is the higher capex for logistics partners. Jumia does not offer financing but does connect drivers with lenders. Thus, I expect a slow adoption of EV-based deliveries across Jumia’s markets.

Kenya

Kenya is another important component of Jumia’s growth story. The playbook for expansion looks the same as in the Ivory Coast and Nigeria, where upcountry growth is a core part of Jumia’s success. Dufay estimated that Kenya “should be slightly bigger than the Ivory Coast” in share of the company’s GMV. Kenya is currently 17% of Jumia’s GMV; the Ivory Coast is 24%. Kenya’s physical goods GMV grew 49% year-over-year versus 44% year-over-year growth a year ago.

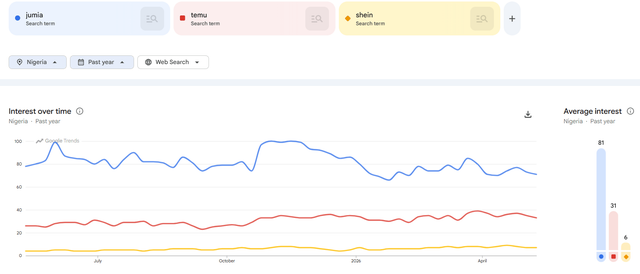

Competitors

Jumia’s competitive landscape has become a bigger part of the discussion in recent quarters. The company’s business model has proven resilient and more capable of delivering trusted goods at acceptable price points. The recent disruption in global supply chains further revealed the competitive strength of Jumia’s logistics. During the earnings conference call, Dufay noted that “the recent disruption of air freight going through the Middle East is expected to create headwinds for non-resident platforms that rely on direct international shipping.” Jumia’s competitors cannot switch from air freight to sea freight because they rely on shipping direct to customers. These customers will not wait for a ship to arrive with their goods. Jumia’s inventory and logistics management has become a distinct advantage during this time.

Dufay further explained that “we have all the products on the ground, and it’s all sea freight. So it’s definitely cheaper.”

While this upside is temporary, I expect this episode to further strengthen Jumia’s brand, especially relative to the competition.

AI Transformation

Jumia’s technological transformation continues to take shape. The company is now formalizing previously organic AI development into structured company-wide initiatives. Dufay explained that Jumia has embedded AI “in pretty much every function,” and each function is taking ownership. During an extended period of discovery, Jumia staff used AI in creative ways for producing various solutions. Dufay described cost efficiencies like “building apps that make sense that give big shortcuts compared to usual tech development.” The company “has been able to speed up and automate lots of things.” Dufay listed benefits such as faster data reporting, databases integrated with Claude, automated compliance, and automated accounting.

Dufay declared that this AI-driven transformation is “just the beginning.” He sees great potential. Thus, Jumia will continue to streamline its cost structure on the way to profitability next year. In future quarters I want to see the transformation move from cost savings to revenue generation given the compounding effect of growth drivers.

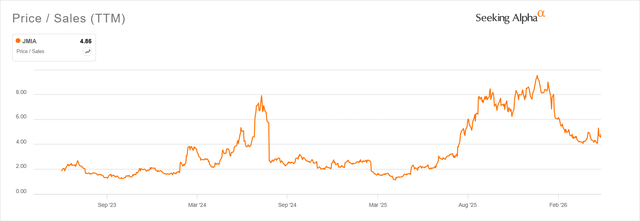

Valuation

Trading at 4.9 times 12-month trailing sales, JMIA is not expensive and priced for perfection. However, it is also not a bargain like it once was.

Still, at current levels I rate Jumia as a strong buy. I remain focused on Jumia’s potential to become a major e-commerce player in Africa, with the 2030 plan becoming a major roadmap for achieving success. Absent greater destructive disruptions in the global economy, I expect JMIA’s low for the year (around $6.40) to hold as support. If I had not already added more shares during this year’s sell-off, I would buy shares around current prices.

Conclusion

The U.S. environment for retail is getting tougher with inflation pressures and economic uncertainty. Jumia Technologies (JMIA) has weathered these kinds of pressures and more while steadily and persistently building a resilient e-commerce business in African markets. Yet, the stock market has exhibited a fresh skepticism about the company’s prospects. Last year’s 2030 plan received an initially tepid welcome. An eventual rally into and through a successful Black Friday season was disrupted by a 16% decline in response to Q4 earnings. The stock has yet to recover from this decline. Even last week’s post-earnings surge was quickly reversed in 2 trading days.

Yet, this tentativeness creates the latest opportunity for making a bet on African e-commerce. As always, this bet is not for the faint of heart, but the good news is that Jumia’s core story and compelling narrative have trended better and better despite all the volatility of the past three years. CEO Francis Dufay has a clear strategy and vision for the company, and quarter after quarter the company builds additional momentum through excellent execution.

Thus, I remain bullish on the stock with an eye to the company’s forecast for profitability and cash flow positive as the milestone, which should introduce the company and stock to a new cohort of believers and buyers. I consider this period an opportune time to position ahead of this coming achievement.

Author

Dr Duru

Ahan Analytics

About Jumia

Jumia is a leading e-commerce platform in Africa. Our marketplace is supported by our proprietary logistics business, Jumia Logistics. Jumia Logistics enables the seamless delivery of millions of packages.

Follow us on, Linkedin Jumia Group and X @Jumia_Group

For more information about Jumia:

Abdesslam Benzitouni

[email protected]